Germany and Canada’s recent policy choices are not merely tactical responses to domestic industrial pressures. They reflect a sober recognition of a rapidly evolving global automotive order. With the “green light” now on, the rules of the game are quietly being rewritten.

At a recent press conference, Germany’s Environment Minister Carsten Schneider struck a measured but firm tone. “Whether in the data or on the streets,” he said, “I see no sign of Chinese carmakers flooding the German market.” Behind this remark lies a clear signal: Berlin is opening its policy door to Chinese electric vehicles.

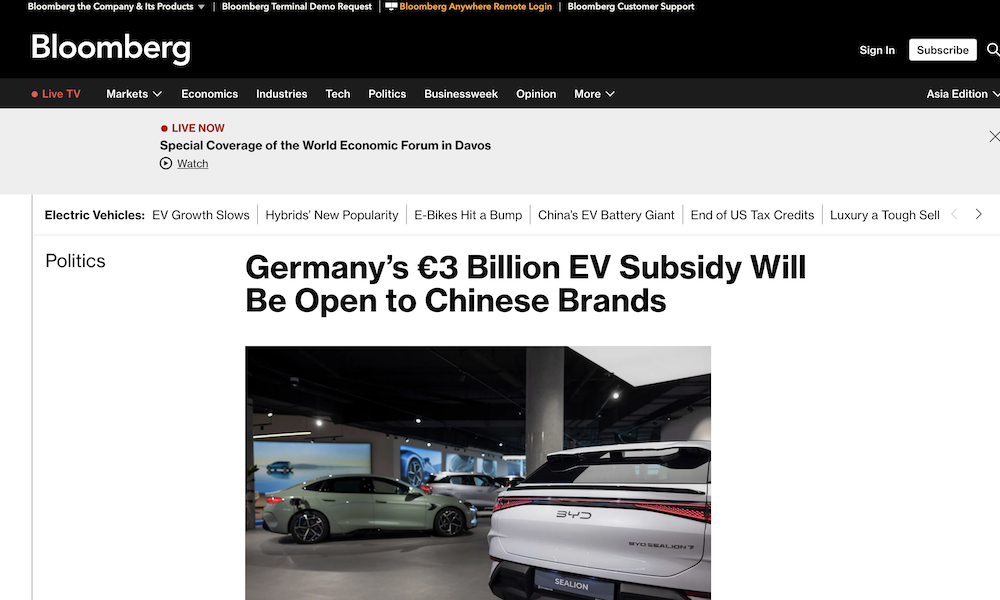

In a bid to revive sluggish EV sales, the German government has announced the relaunch of a €3bn electric vehicle subsidy programme over the next three years. Crucially, the scheme will be open to all manufacturers, including Chinese brands.

Almost simultaneously, during a visit to Beijing, Canadian Prime Minister Mark Carney confirmed that Ottawa would scrap the 100% additional tariff on Chinese electric vehicles. In its place, Canada will introduce an annual import quota of 49,000 vehicles, within which cars will be subject to a most-favoured-nation tariff of just 6.1%.

These seemingly abrupt policy shifts are far from simple gestures of trade goodwill. Under pressure from industrial transition, climate commitments and market realities, the global automotive sector is gradually moving away from confrontational protectionism towards a more pragmatic phase.

The Reality Behind the Green Light

As one of the traditional powerhouses of the global automotive industry, Germany is encountering clear bottlenecks in its electrification drive.

Launched in 2016, Germany’s original EV subsidy scheme once provided strong momentum. But mounting fiscal pressure forced the government to terminate the programme at the end of 2023, triggering an immediate market downturn. According to data cited by People’s Daily, registrations of battery electric vehicles in Germany fell by 27% year-on-year in 2024, to just 380,000 units—well below government expectations.

At the heart of the slump lies a familiar problem: price. With subsidies removed, the cost gap between electric and internal combustion vehicles widened once again. At the same time, most electric models offered by German manufacturers remain concentrated in the mid-to-high-end segment, typically priced above €30,000—well out of step with mainstream demand.

Germany’s consumer structure has long made affordable models essential. Middle- and lower-income households account for roughly half of new car buyers, and are highly price-sensitive. For them, vehicles priced above €30,000 exceed both psychological thresholds and practical budgets. Minister Schneider addressed this directly: “German carmakers have strong and competitive product portfolios, but consumers also need vehicles that fit their budgets.”

Against this backdrop, reviving subsidies became inevitable. This time, however, Berlin has abandoned geographical restrictions. The €3bn fund will be open to all manufacturers and will even cover range-extender EVs. Subsidy levels will range from €1,500 to €6,000, depending on vehicle type, household income and family size.

The logic is straightforward. Thanks to their cost advantages, Chinese manufacturers can push post-subsidy prices down towards the €20,000 range—precisely the segment left underserved by domestic brands. For Germany, this is a practical lever to accelerate EV adoption and meet climate targets.

Schneider’s insistence that he sees no “flood” of Chinese cars reflects both confidence in Germany’s premium offerings and an implicit recognition of the complementary role Chinese affordable models can play. By 2029, the government hopes the subsidy scheme will help put around 800,000 electric vehicles on German roads.

Canada’s situation, however, is more complex—and its policy pivot carries a stronger sense of urgency.

For decades, Canada’s automotive industry has been deeply dependent on the US market, which absorbs around 90% of its vehicle exports. That dependence turned into a liability in 2025, when Washington imposed tariffs on Canadian-made vehicles and components.

The impact was immediate. General Motors halted production of BrightDrop electric vans at its CAMI plant in Ingersoll, Ontario, and scaled back operations in Oshawa. Stellantis shelved plans to produce the Jeep Compass at its Brampton facility near Toronto, shifting capacity instead to Illinois. Thousands of jobs were put at risk.

Compounding the problem is the near absence of a domestic EV industry. Canada has no electric vehicle assembly plants with annual capacity above 50,000 units, and less than 8% of key components are locally sourced—leaving the country without the industrial foundations needed to independently drive electrification.

Canada had set a target for new energy vehicles to account for 20% of sales by 2026. But tariff barriers and limited model availability forced the goal to be postponed by a year. In 2025, pure EVs accounted for just 8–10% of sales—far short of expectations.

Against this backdrop, Chinese EVs stand out for their pricing power. Compared with vehicles of similar size and range, Chinese models are typically US$10,000 to US$15,000 cheaper. Cooperation with China, in this context, has begun to look less like a choice and more like a necessity.

Who Stands to Gain?

Although Germany and Canada have effectively switched on their policy “green lights” at the same time, the nature of the opportunity differs markedly between the two markets.

Germany’s subsidy scheme is universal, applying equally to all brands. This creates a direct entry point for Chinese manufacturers known for value-for-money offerings. Chinese brands have already begun to make quiet inroads. In April 2025, BYD sold 1,566 vehicles in Germany—up 120% year-on-year and well ahead of Tesla’s 885 units. Leapmotor’s T03, priced from €18,900, could fall to as low as €13,000 after subsidies, neatly targeting the €20,000 segment. MG and others are also expanding rapidly, filling gaps left by domestic brands.

Canada’s opportunity, by contrast, is more stratified. Under the new policy, China is granted an annual quota of 49,000 vehicles at reduced tariffs. Within five years, Ottawa hopes that half of these—around 24,500 vehicles—will be priced below C$35,000, to address the shortage of affordable EVs.

Tesla already has a strong foothold in Canada, with 39 stores and a mature sales and charging network. It is well positioned to absorb the non-affordable half of the quota. However, its cheapest Model 3 still exceeds the C$35,000 threshold, effectively excluding it from the affordable segment.

For Chinese manufacturers, Canada’s real value lies further ahead. The government has made clear that over the next three years it intends to build a domestic EV industry through joint ventures and strategic investment with Chinese firms, while drafting a new automotive strategy that could disadvantage companies without local production.

In other words, simple exports will not be enough. Deep integration into the local industrial chain will be essential.

Some Chinese companies have already moved early. BYD entered the Canadian market in 2013 and opened an electric bus assembly plant in Ontario in 2019, supplying transit authorities in cities including Toronto and Vancouver. Geely, meanwhile, could leverage the brand synergies of Volvo and Lotus. Lotus CEO Feng Qingfeng has publicly welcomed Canada’s policy shift.

Canada’s rich reserves of lithium and cobalt also complement China’s mature battery supply chain. Through a combination of technology transfer and resource cooperation, Chinese manufacturers could establish localised production systems—shifting from product exports to industrial roots.

A Turning Point for the Global Automotive Industry

As electrification and intelligent mobility reshape the industry, the old competition model built around regional barriers is gradually eroding. In its place, a new order—centred on technological innovation and supply-chain capability—is taking shape. The global automotive sector is approaching a historic inflection point.

According to the China Association of Automobile Manufacturers, China exported 7.098 million vehicles in 2025, up 21.1% year-on-year, ranking first globally for the third consecutive year. New energy vehicles accounted for 2.615 million units—double the previous year—and have become the primary growth engine.

More symbolically, in April 2025 BYD overtook Tesla in monthly sales across 14 European countries, leading in key markets such as Germany, the UK and Italy. The long-standing dominance of foreign brands in Europe’s EV market has been decisively broken.

Germany and Canada’s policy shifts can be seen as recognition of this reality. China has built a complete EV ecosystem, spanning raw materials, core components, vehicle manufacturing and charging infrastructure. This end-to-end advantage has become impossible for the global industry to ignore.

European media sentiment has begun to reflect this shift. Germany’s Handelsblatt noted that even with tariff barriers in place, Chinese car sales in Europe have continued to rise, with no evidence of dumping. On the contrary, brands such as BYD and MG are often priced higher in Europe than in China.

Swiss outlet Watson has cited automotive experts who argue that European consumers are increasingly receptive to Chinese brands, largely because they deliver practical, well-equipped and intelligently designed products that closely match market needs.

Together, these signals point to a fundamental rewrite of the competitive rules. Success is no longer determined by tariffs or brand protection, but by sustained innovation, supply-chain efficiency and the ability to respond quickly to consumer demand in open markets.